Recent Developments Across India’s Defence-Tech Companies - Astra, Azad, Axiscades, and HBL

Disclaimer: This is not a buy or sell recommendation. I’m not a SEBI-registered investment advisor, and nothing shared here should be taken as financial advice. This content is purely for educational and informational purposes. I’m not affiliated with SEBI or any brokerage, nor am I trying to promote or sell anything. Always do your own research before making any investment decisions.

This whole piece I wrote is based on the recent one-year movement of these companies - what they’ve done so far, with references from their concalls and new data.

It’s not like the detailed deep dives I did earlier on Sanghvi Movers or GPIL. This one is more of a mix, because a lot of members have been asking me about these specific companies.

Since the new quarterly results are coming soon, I decided to focus only on the main parts, not go too deep into micro-level details right now.

Still, I think I’ve covered around 90% of the important stuff - enough to understand what’s really happening inside these companies at this stage.

Astra Microwave

Astra Microwave started FY26 with strong momentum. Its Q1 standalone revenue was ₹197 crore, a 28% year-on-year rise, and margins improved sharply. The order book stood at ₹1,891 crore by June 2025 - now it cross to 2,000 crore, providing clear visibility for the coming quarters. Management expects steady to slightly higher profitability this year because the company now focuses on high-value domestic projects and has reduced low-margin “build-to-print” work.

In August 2025, Astra won a ₹135-crore DRDO radar upgrade contract, adding to earlier July wins of ₹150 crore, with another ₹250 crore pipeline. Total orders booked so far in FY26 are ₹260 crore, and the company is confident of meeting its full-year inflow target of ₹1,300–1,400 crore by March 2026. The main growth driver is a steady flow of radar, space, and chip contracts.

Its joint venture Astra Rafael Comsys (ARC) - Israeli company - holds ₹400-crore orders and aims for ₹350-crore revenue this year at roughly 10 % PBT margin. ARC could secure ₹800 crore more in FY26, including three SDR contracts worth $100 million before March 2026, where management says the win chance is “100 %.” Despite some Q1 supply-chain delays, ARC is expected to meet its annual plan.

Management says defence reforms - higher FDI limits, local design mandates, better testing infrastructure, and “Make in India” procurement - are expanding opportunities for private tech players like Astra.

Business Transformation

Major Segments

IF I CONCLUDE EVERYTHINg

short term, near term and long term :)

Challenges and Risks

AZAD ENGINEERING

The company began FY26 with its best-ever start, earning ₹135 crore revenue, up 36.7% YoY, helped by higher production, new capacity, and new plant approvals.

EBITDA margin rose from 33.6% to 36.1%, and PAT margin improved from 17.4% to 22.3%.

It has a strong order book of ₹6,000 crore+, giving solid visibility - led by energy sector (~₹3,400 crore), aerospace & defence (~₹1,700 crore), and oil & gas (~₹850 crore).

It has planned ₹1,450 crore capex for FY26 to expand capacity and stay ahead of demand. Subsidiaries bought last year are now EBITDA positive and will boost profits from FY26. The company expects 25–30% revenue growth this year and is confident it may cross that. Its focus is on high-margin niche markets, especially exports (40% of revenue), mainly to the US.

Management said there’s no major raw material or capacity issue, and growth is aligned with demand. Most orders are long-term, especially from energy, aerospace & defence, and oil & gas, giving strong multi-year revenue visibility. No tariff risk expected since pricing is transparent and cost-efficient. The company does not plan to enter low-margin or commodity segments. It’s exploring new export markets, beginning with Hyderabad expansion before going global.

Hiring has been steady; employee costs rose slightly as workforce grew to match new capacity. Its strategy focuses on consistent growth in revenue, EBITDA, and PAT through expansion and efficiency. With strong cash flow, capex, and rising demand, management expects growth to accelerate as plants stabilize.

The management talked about many risk areas during the earnings call - mainly around operations, markets, pricing, geopolitical issues, and customer concentration.

They also explained how they are handling these risks through strategic actions and planning.

They mentioned - “We expect challenges to continue for a few more quarters but aim to stabilize operations soon.”

Order Book and Revenue Visibility:

The company’s order book is about ₹6,000 crore, with steady visibility from energy, aerospace, defense, and oil & gas segments. Management said all these are long-term contracts with firm commitments for the next 4–5 years.

They stated, “Our order book is based on confirmed contracts that convert into purchase orders, giving strong visibility for years ahead.”

AXISCADES TECHNOLOGICS

Overall Business Performance

The company earned ₹244 crore revenue in Q1 FY26, up 9% YoY.

EBITDA was ₹34 crore, same 14% margin as last year. If we remove one-time ESOP cost, EBITDA grew 86% to ₹34 crore from ₹18 crore. PAT rose 25% YoY from ₹17 crore to ₹21 crore.

Management expects faster growth in H2 FY26 led by defense ramp-up and better margins. Core business (defense, aerospace, ESAI) grew 17% to ₹182 crore (from ₹156 crore). Company is building capacity for long-term growth, targeting 40% CAGR in core verticals and ~19.5% EBITDA margin by FY28.

Defense

The defense order book is ₹540 crore, with projects from DRDO, PSUs, MBDA, and Indra. Total confirmed defense orders for FY26–27 stand at ₹1,500 crore.

Most execution will happen in H2 FY26, extending over two years. Work includes OEM contracts, counter-drone, and tank trailer systems.

The book is diversified, not dependent on any single project. The company is working on mountain radar systems and BrahMos missile electronics (like wiring and control systems). Defense revenue is expected to grow strongly in H2 FY26 as deliveries pick up. The segment has long-term stability, with strong visibility and no current dependency risk.

RISK: Customer Concentration and Diversification

RISK: Talent Attrition and Workforce Stability

They are investing in training and upskilling to reduce outside dependence.

They partner with external experts to retrain workers and lift output. Employee engagement efforts continue to reduce attrition. They aim to improve productivity steadily over the next quarters.

RISK: Infrastructure and Capital Expenditure (Capex) for Growth

RISK: Market and Competitive Risks in Core Domains

Management on Latest Concall

IF I CONCLUDE EVERYTHING

(Next 1 to 2 Quarters)

Cancelled or Postponed Initiatives

Management Tone on Projects

HBL ENGINEERING

Chairman’s Address - Dr A J Prasad

He said he would speak on four main topics before taking questions:

Business prospects for the next few years.

Company’s focus on high-tech niche markets.

Product mix and diversification.

Use of surplus cash.

1️⃣ Business Prospects (Next 3 Years)

He admitted India’s economy is becoming uncertain but said visibility for the next three years still exists unless something unexpected happens. Last year’s report had predicted flat sales for FY25 - that proved true, with a small decline.

Main reason: delay in Kavach (train safety system) orders.

Every month of delay in government orders pushes deliveries ahead.He recalled an investment banker once said HBL deserved a “20% conglomerate discount.” Dr Prasad countered that HBL instead deserves a “portfolio premium.” Each division earns profits on its own; none hide losses. Railway signalling is totally different from batteries, yet diversification worked because HBL took long-term R&D risks others avoided.

YESTERDAY HBL GOT UPGRADE IN CREDIT RATING 10 OCT 2025 :)

CENTUM ELECTRONICS

The order book as of June 2025 was ₹1,769 crore, supported by new EMS customers that entered serial production after completing NPI qualification. The company continued to expand in its core high-margin BTS business, focusing on defense, aerospace, and space programs.

The domestic BTS order book was ₹886 crore, with margins around 14–15% and potential to improve further. Management expects BTS revenue to grow by around 25–26% annually over the next two to three years, and even faster if large tri-services or platform orders are secured.

Programs like DRDO’s Virupaksha Radar are currently small (around ₹10 crore) but can scale up to ₹200–300 crore platforms once they move into production after qualification. BTS projects usually take 18–24 months from design to execution.

The Engineering and Manufacturing Services (EMS) segment serves multiple sectors such as defense, aerospace, industrial, energy, medical, and automotive. The EMS order book stood at ₹710 crore, spread across clients in the US, Israel, Malaysia, and Singapore. The company expects 18–20% growth at the consolidated level with a ₹40 crore CAPEX plan in FY26 to expand capacity and efficiency. Margins in EMS are lower but stable, depending on product mix and order timing.

MY POINT OF VIEW

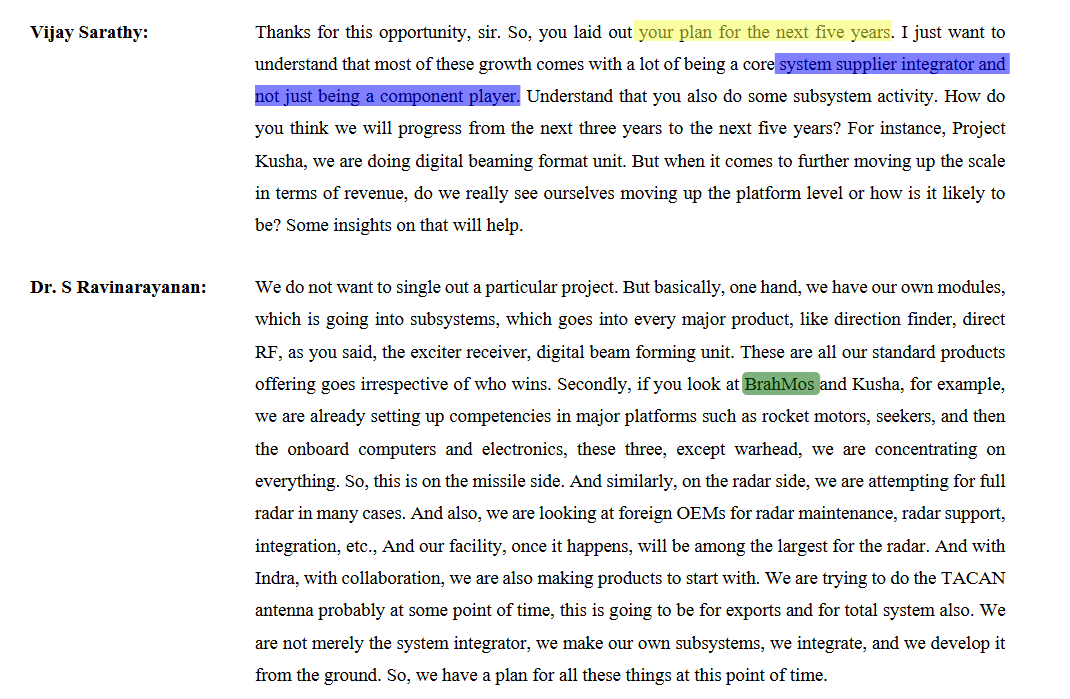

When you look deeper into India’s defence ecosystem, the real game is about who is moving fastest from just being a component supplier → to a system integrator → and finally to a technology owner.

Now, if you zoom out to the macro picture, India’s defence ….

So, the smart play is either:

Buy strong businesses at reasonable valuations, or

Do short-term swing trading with strict stop-loss and alert system.

You can also look for neglected but fundamentally solid companies, where there’s temporary negativity — that’s where big money hides.

Personally, I think companies like Avantel, CFF Fluid, and Krishna Defence are also very interesting - niche, small, focused - but worth studying more.

This is just one trick of the whole buy-and-sell strategy.

I’ll also share what I found on NotebookLM, so definitely go through that - don’t ignore it. That’s it for now. Bye!

If yu want to Read Full Article :)

Support my writing and get full access to every post, archive, and exclusive insights directly on Buy Me a Coffee.

👉 Read the full post here

Already a supporter? Just log in to your Buy Me a Coffee account to continue reading.